Growth is (a) Discipline

This is a heavily redacted transcript of a talk by the same title I held together with my friend and colleague Uli Schmitz at the 2025 High-Tech Gründerfonds (HTGF) Family Day in Berlin.

TL;DR: Limited later-stage funding in Europe necessitates a focus on competitive scaling with fewer resources. Data suggests it is possible, but it requires an educated choice and consistent application.

Europe is at a later-stage funding disadvantage compared to the US. There are a couple of reasons for this, mainly:

- There is simply more money in the US Venture Capital (VC) ecosystem,

- The majority of it gets deployed in later stages, in contrast to Europe and Germany, where the majority of investments are early-stage, and

- Tier 1 US VC firms, in particular, have bigger funds, allowing them to sign a greater number of larger tickets.

This is an issue because while money cannot buy success, it can - and it does - buy growth. Usually by way of (growth) marketing, sometimes through M&A activity, and often through outsized talent acquisition or frontloaded organisational growth. Let’s call this expedited growth, and if growth tactics had slogans, its slogan would be SPEND FIRST TO SCALE FAST. If you choose to scale this way, less funding puts you at a substantial disadvantage. Yes, you can try to execute better, but it’s hard to compensate for a lack of fuel if you run the same engine.

And the lack of later-stage funding is particularly painful because expedited growth is particularly relevant in the scaling phase of a company - when you have a product that resonates so well with customers that scaling becomes the biggest problem to solve.

Why is this a problem? Well, first of all, it means that EU founders cannot rely on funding to compete well in the scaling phase. Yes, you can attract overseas capital as a European, but it’s way easier for US startups because there are fairly strong network effects in Venture Capital. And secondly, when European startup do manage attract US capital in later stages it not great for our ecosystem, because it means that IP created here (based on European Funding) will predominantly generate value overseas.

And so, hardly surprising, this later-stage funding inequality is being lamented quite a lot, and various initiatives exist to close this gap at least to some degree. But the former is useless, and the latter will take a while to make a meaningfully equalising impact, so I think it’s useful to think about what can be done today to be competitive despite the gap: How can you scale competitively with less money?

Well, logically, there is only one answer to it really: you need to build a different kind of engine, one which requires less fuel by design, because it prioritises efficiency over torque. In other words, you need to apply growth tactics that prioritise capital efficiency. Let's call this efficient growth, its imperative would be EARN EARLY AND SCALE SMART, and its core basic principles can be summarised as follows:

o You focus on revenues already with your first marketable product. If people are not willing to pay for it, it’s not worth pursuing. Customer activity or “engagement” is not enough. Also, you really care about price points and perceived value. You balance growth and margins. In particular, your leading KPI for performance marketing cannot be revenue, but contribution margin 1 (revenue minus the cost of marketing or the costs of goods sold, COGS, depending on your business model).

o You are very focused and disciplined with your burn - you act (and test and iterate) based on a strategy (if you are unsure what that term means exactly please continue reading here, and forgive me for being self-referential) and you invest people and time only on your biggest bet, on your long-term goal. You avoid getting sidetracked by opportunities. You say no a lot. You run as little activity in parallel as possible. There is no such thing as “multiple initiatives”.

o You are very considerate about growing your organisation: you avoid any under-utilisation and rather leverage scarcity as a means to reinforce focus: you don’t speed up problem solving by adding people, but by reducing complexity and activity. And you scale with clarity and foresight to build an organisation that is efficient in the long run – we’ll get into what this entails a bit further down below.

What this does NOT mean is that you aim to grow more slowly than if you were to follow expedited growth tactics instead. But your acceleration curve is different. Let’s imagine two runners to illustrate what I mean: The expedited growth runner explodes out of the starting blocks and takes the first half-lap dominantly. But the quick start comes at a cost. The big sprinter legs of the expedited runner are less capable of maintaining speed. Lactate builds up. The bulk starts to slow him down. And this is the time of the efficient runner. He has maintained his energy, he has skinny, slow-burning muscle and is more lightweight than his competitor. And he now starts to catch up. And eventually he’ll get to the line first.

What a cute fable, you might say, but how about some real-life examples, huh?

Challenge accepted.

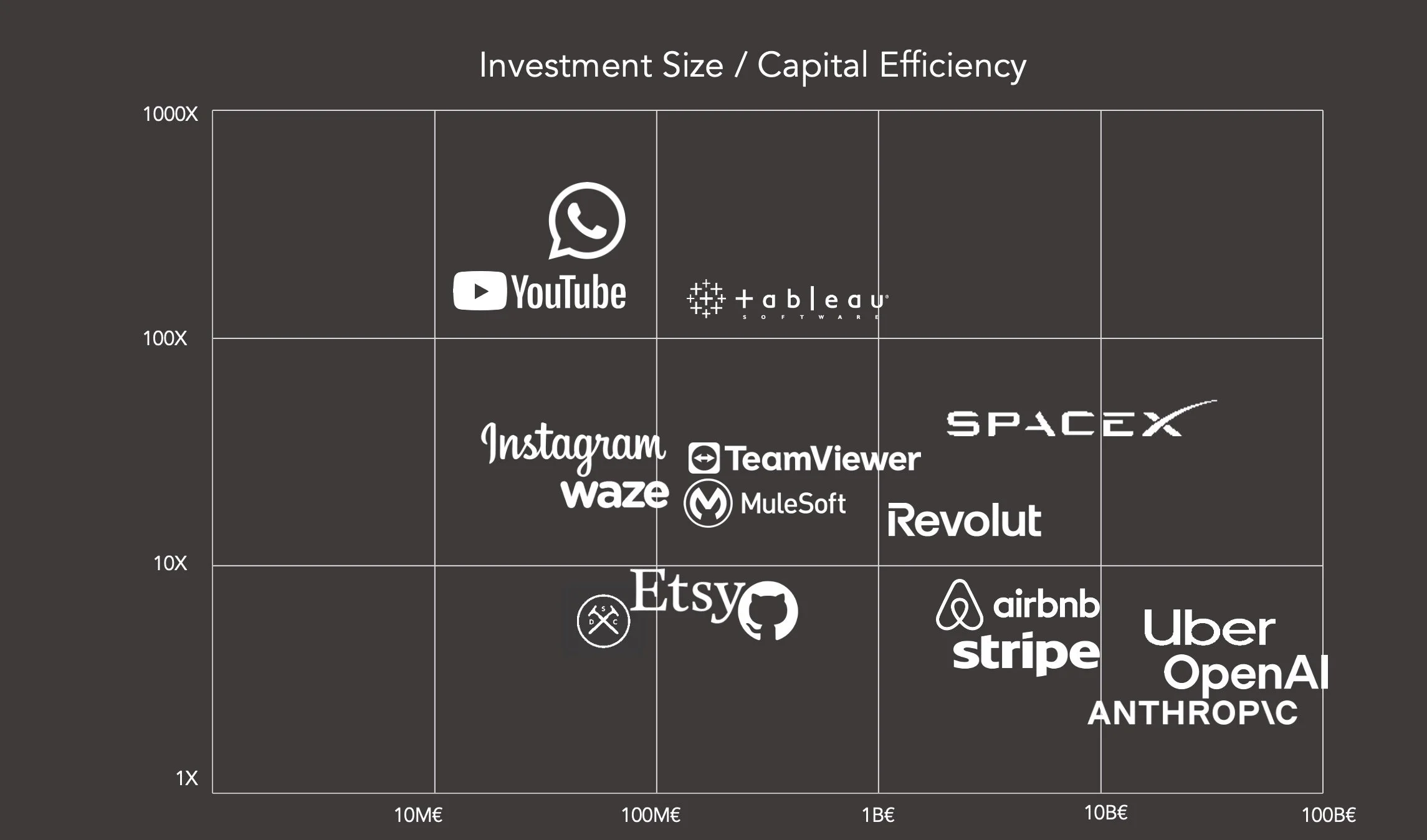

We have looked 29 unicorns of the last decade, amongst of which are the follwing:

We have then compared their funding (x-axis) with how much money they have returned per $ invested (y-axis):

Note, that both axis have a logarithmic scale

- The X-axis shows how much funding a company has raised before an IPO, or in lieu of that, an acquisition or, if neither has happened until today, the current market valuation per the last known round of financing (the valuation event)

- The Y-axis shows the valuation determined by said valuation event as a multiple of the funding until that point in time.

The source of all data is PitchBook.

Now, for better readability, let’s look at just the datapoints of the full roster of companies and add a regression line.

If the eagle-eyed among you are wondering why there are 28 dots representing 29 companies, that’s because we’ve taken out We-Work as an outlier, which would have made the regression line fall even steeper.

Interesting, huh? The return on investment decreases with more funding. The companies with less funding returned more money on the $. The slow starters win.

Ok, maybe that’s an overstatement. Because, in all honesty, this analysis is well short of scientific proof. First of all, we are sometimes comparing apples (IPOs) with pears (acquisitions). Secondly, the timing plays a huge role in valuations, and we have not normalised for it. Thirdly, for some companies, like Open-AI and Anthropic, the bet is still open and may result in extraordinary returns.

But at a minimum, I think this shows that we cannot assume that more funding systematically creates outsized returns.

Also, there is this analysis by Sifted, according to which European VCs produce higher IRRs than their US counterparts, despite the money gap. Again, this does not prove our findings right, but it does shed a supporting light on them.

Sidenote: Are relative returns the right metric? Shouldn’t we be looking at absolute returns / absolute valuations? Because - full disclosure - according to our data , more funding does indeed result in higher absolute valuations.

Logically, yes, absolutely, it is the right metric. Capital under management is always finite, and so what you make of it, the relative returns, is what matters. And VCs do indeed usually use relative KPIs such as cash-on-cash multiples or Internal-rate-Of-Return (IRR) to evaluate performance. But according to this study (bottom of page 7) most VCs believe that - in contrast to their own thinking - their investors care more about absolute returns.

In any case, two groups of people should definitely focus on relative returns (off of limited funding) instead of absolute returns (off of less limited funding), and these are founders and early-stage investors. Because for them, less funding means less dilution. So I do think we are looking at the right metric after all, at least relating to people I care about the most.

So for now, let’s just say, that both expedited growth and efficient growth can lead to successful growth and attractive returns. Both are proven growth tactics.

But this is not the point of this post, though. No Madam. The point is that there is no promising middle ground between them.

Let me explain. The principles of expedited and efficient growth are opposed. This is true for all three mechanisms of expedited growth, growth marketing, M&A and organisational frontloading, but I think it can be explained best when we look in more detail into the last: organisational growth.

If you choose expedited growth, you want to create the maximum effect as soon as possible. Accordingly, you hire as fast as you can, and this usually means you hire on all levels at the same time. You accept that the organisational structure is in constant flux because of the dynamic and breadth of this growth. Also, you have a management bias: you tell people what to do so that they generate output quickly.

If, on the other hand, you choose efficient growth, you are more concerned with maintaining speed in the long run. So you try to build a structurally sound organisation: You will hire from the top. You will not staff a team before you have leadership for it. You anticipate when you need to level up structures and you try to keep them as stable as possible in the meantime, because you know how much friction and naval-gazing structural changes cause in an organisation. And you have much more of a leadership focus, meaning that while you do direct people at times, you also make sure that they have discretion and room to exercise their responsibility and grow.

You have a people-centred view. You see people as a long-term resource, and you know that developing your talent into ever greater responsibilities is incredibly efficient. Accordingly, you hire with attention to fit and potential. You want to keep people, and you focus on their integration, retention and development. You encourage multi-dimensional career paths because people who understand the company from various points of view are the best agents of alignment for a larger organisation.

In contrast, if you seek expedited growth, you have more of a position-centred view. You want to fill positions quickly and so you prioritise experience over potential. You are more interested in having vertical career paths, because transitions are easier and quicker (same basic experience). And of course, you have a hiring priority over a retention priority because it gives you more bang now.

Cheat Sheet

So, opposed principles indeed. But the two growth tactics are not opposites of each other; they are also very consistency-dependent within themselves: you lose out on their respective benefits if you are not consistent. Having an organisation that is neither particularly fast out of the gates nor particularly efficient in the long run is the worst of both worlds.

And this is the second point that I wish to make with this post: expedited and efficient growth don’t mix. You need to make a conscious choice about which growth tactic you will pursue and stick to it.

But be aware of cognitive bias when you make that choice. Because expedited growth is much more comforting for our brains. And our brains like comfort (read “Thinking, Fast and Slow” by Daniel Kahneman if you don’t believe me - and if you do believe me but haven’t read it yet, read it anyway!) and therefore have a tendency to lean towards expedited growth.

There are two reasons why expedited growth feels more comfortable:

1. In expedited growth, you scale primarily based on funding, i.e. money that you already have, not money that you are yet to make from the customer. That means you can focus on the execution of spending. And over that, you have control. You do not have control over incoming revenue. Because that is driven by customer choice, and you cannot control that. This is the same reason why planning feels good and strategy feels risky. You control cost. You do not control the customer. So if you focus on spending, you can focus on things that you can control!

2. Action bias. We like activity – particularly in uncertain circumstances. Founders like to start things. And Investors like founders who seem to have limitless energy, who seem driven to action, who never rest. It’s irrational because activity by itself really only means burning fuel – it is not a good thing per se. But if you’ve just received funding, you probably feel that you owe it to the people who just gave you money that you are not just sitting on it. And if you’ve just invested in a company, wouldn’t you want to see a demonstration that your investment is being put to use? Activity is comfort: something happens.

In summary, we like expedited growth because we feel more in control and there’s a lot of action.

But the comfort that expedited growth provides is a fleeting sensation. And the reason for that is organisational debt. Organisational debt accrues whenever you have too much population for the supporting structures, utilities and order. Picture an overpopulated city. Everything becomes laborious, people are stressed, mundane tasks take forever. As the term “debt” insinuates, organisational debt never goes away by itself (it needs to be paid back) and it carries interest. It gets worse over time. It causes more and more friction, wasting the organisation’s energy, frustrating it and slowing it down. If you choose to grow your organisation expedited, you pretty much always build up organisational debt. You hire first and adjust structures and processes afterwards. And you usually don’t find or take the time to pause and structurally fix the many small things that got broken on the way. You keep pressing forward and (consciously) live with the inefficiencies. But believe me, running an indebted organisation is way less fun than running an efficient one. Things get lost all of the time. People are frustrated a lot. Everything seems to take ages. And changing into an efficient organisation now is difficult. Because the basis for efficiency is missing. You need to get to the foundation and straighten things out. This takes a lot of time, effort and willpower. In essence, it’s a restructuring. No fun.

So be aware of your cognitive bias. And not only when you choose a growth tactic. But also - and this is very important - when you have chosen efficient growth. Because the same bias that has made the choice more difficult will likely try to undermine your consistent execution. Everybody likes efficiency. But we do not like to focus and let opportunities pass. And this would be the last point that this post wishes to make: Growth is a discipline. You need to choose with clarity. And efficient growth requires discipline. You cannot have the cake and eat it too. You cannot want efficiency and lots of activity and chasing of opportunities.

I said initially that this post would be about what can be done today in order to grow competitively despite the later-stage money gap. And so, to close the loop, here’s my practical advice… or maybe rather my plea:

First of all: keep thinking. Do your own research. Make up your mind about efficient vs. expedited growth as a growth tactic of choice. Think about what its advantages and disadvantages mean to you, your company, your business model or portfolio and market. Reflect on how you feel about them. And if you think that it’s worth making a conscious choice about how to grow…

… then make it a talking point with your investors, or if you are an investor, make it a talking point with your founders. Actively grappling with the concept of growth tactics, having the same understanding of what they each entail, what their respective pro’s and con’s are, and what is easy or hard about them, and aligning or agreeing on one helps a lot in the consistency department.

I don’t think these kind of discussions and agreements happens nearly enough today. And that we will be able to build more winners if we improve on this.